Keeping Your Car in Bankruptcy.

You don't have to lose your car when you file for bankruptcy. The Value of the car is the first point of consideration. Each year, the Australian Financial Security Authority (AFSA) sets the maximum value for a vehicle you can own during bankruptcy. In 2019, that amount is $7,900. 00. If the car is joint them its $ $ 15,800.00. This amount is based on what a dealer would pay to buy the vehicle from you, not the amount you would pay to buy the car. This calculation also takes into account how much is still owing on your car loan.For example, if you own a car that is worth $30,000 and you still owe $25,000, the calculated value would be $5,000. This would fall under the limit, allowing you to keep your vehicle. If, on the other hand, you only owed $5,000 on that $30,000 vehicle, the value would be $25,000. In this case, you may be required to sell the car to cover your outstanding debts. You would, however, still be eligible to keep the $7,900 set out in the limit so that you could purchase a less expensive car. Joint Ownership of Car. In some cases, you may own a vehicle in partnership with someone else. Only your own portion of the vehicle, value would be used in determining whether or not you are allowed to keep it. If you are not allowed to keep your share of the car, either the other owner would have to purchase your portion from you or you would be required to sell the vehicle and split the proceeds. 5/5/2019 Bankruptcy and the home Is the home protected?

No. What about joint ownership? The bankrupt and their non-bankrupt partner/spouse will own the home as ‘joint tenants’. When the bankrupt and a non-bankrupt co-owner jointly own the home, the trustee will have an interest on the bankrupt share. How is the equity in a property determined? The trustee will get the property valued to determine the equity. Secured debts (e.g. mortgages, etc.) are deducted from the property’s value and the bankrupt’s share of the equity is calculated. What if there is no equity in the property? When there is no equity in a property and the debts secured against the property are greater than the current property value, the lender may exercise their rights and sell the property. If lender don’t exercise their rights, the bankrupt and possibly other parties can continue to service the loan. It is also reasonable to expect the property’s value to increase. The property vests in the trustee at the time of bankruptcy and remains vested regardless of whether the trustee takes action to sell the property, or when there is no equity in the property. The property remains vested in the trustee when the bankrupt has been discharged from bankruptcy. The trustee will generally review the property’s equity position periodically. They can realise any equity generated after the date of bankruptcy, even if the equity has been generated by the continued mortgage repayments by the bankrupt or another owner. Mortgage repayments attributed to the bankrupt’s share are deemed to be rental payments to use and occupy the property. How are properties realised? Where the trustee is the only owner, they can put the property up for sale. Where there is a co-owner, the trustee will usually take the following approach:

What if the bankrupt can continue with mortgage repayments? If the bankrupt has the capacity to continue making mortgage repayments, usually the mortgagee will not insist upon possession of the property—preferring that the loan repayments continue. The trustee and bankrupt may negotiate payment for any equity in the property to the estate. This type of arrangement benefits everyone concerned: the bankrupt’s creditors benefit from the property’s equity in the estate; the mortgagee retains a performing loan; and the bankrupt’s family avoids losing their home. However, the trustee can sell the property at any time, even if the mortgage repayments are up-to-date. This means that the estate will benefit from the extra equity generated in the property from additional repayments. What about getting vacant possession? Normally, the trustee will need to provide vacant possession when selling a property. A trustee would not usually expect a bankrupt to vacate the property immediately upon bankruptcy; in normal circumstances a few weeks would be allowed for alternative arrangements to be made. In some cases, the trustee may allow the bankrupt to stay in residence during the selling period provided the bankrupt assists in that process, pays a fair rent, maintains the property, and provided the trustee is satisfied of the bankrupt’s continued cooperation in the bankruptcy process. How are the proceeds of sale distributed? If the property is wholly owned by the bankrupt, the estate will receive the entire surplus of the sale after any mortgagee and selling costs are paid. If the property is co-owned, the trustee will share the surplus with the co-owner (non-bankrupt) as per the legal entitlement on the title deed.

1/29/2019 Indexed amounts updated 30 January 2019The Bankruptcy Act and Regulations contain a number of thresholds, limits and other amounts that are regularly indexed (changed in line with the Consumer Price Index or the base pension rate). Release date: 30 January 2019 The Updated thresholds are, Credit limit, amount increased to $5,778.00. Dependants, amount increased to $ 3,642.00. 9/23/2018 12 Month BankruptcyLegislation has been passed through Federal Parliament, such that amendments to the Bankruptcy are now expected with the effect of reducing the duration of a standard bankruptcy from 3 years to just 1 year.

Commencement dates have not yet been announced by the Federal Government, however it is expected 12 month bankruptcy may commence in late 2018 or early 2019. The proposed details around how 12 month bankruptcy will work in practice have not yet been released. Please contact us at any time to discuss how 12 month bankruptcy may work for you.

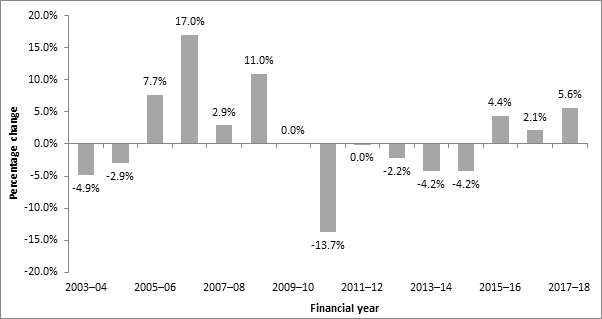

Source: www.smartcompany.com.au The Australian Financial Security Authority today released the personal insolvency activity statistics for 2017–18 and the June quarter 2018. Total personal insolvency activity in Australia: % change compared to the previous year  Spotlight on the June quarter 2018There were 8,177 total personal insolvencies in Australia in the June quarter 2018. This was a rise of 7.4% compared to the June quarter 2017.

6/6/2018 Comments Going Bankrupt with no assetsI have no assets. You do not have to have assets to go bankrupt and you have nothing to loose if you have no assets, except to clear most of your debts. Which debts are not included in bankruptcy;

In this case declaring bankruptcy can be a new beginning & fresh start. The effects of bankruptcy When you become bankrupt

Please call one of our friendly consultants for further information on 1300 942 856 or complete the form below. 6/4/2018 Comments Bankruptcy Application Forms... Where do you go for them ? If you are looking in applying for bankruptcy yourself and looking for the documents, we will be happy to send them to you at no charge. According to the ACCC, Drivers feeling the pinch of high petrol prices should use price cycle information and fuel price websites and apps to shop around, as petrol prices in some cities reached their highest levels in almost four years in May.

Read the full story |